Quick Overview

This explanation focuses on accrual adjusting entries or simply accruals as well as the related reversing entries. (Other adjusting entries such as deferrals are not discussed in detail.)

Accrual adjusting entries are necessary for a company’s financial statements to reflect the accrual method of accounting (not the cash method). The accrual adjusting entries are dated for the final moment of each accounting period and are recorded in the general ledger accounts using that date so that:

- The company’s balance sheet will include all liabilities and assets at the final moment of the accounting period (not simply the amounts recorded from the documents that were routinely processed).

- The company’s income statement will include all the expenses, losses, revenues, and gains that occurred during the accounting period (not simply the amounts recorded from the documents that were routinely processed).

Accrual adjusting entries (as well as all adjusting entries) consist of:

- The date of the final moment of the accounting period (December 31, May 31, etc.)

- At least one balance sheet account (liability or asset account)

- At least one income statement account (expense, revenue, loss, or gain account)

Brief example

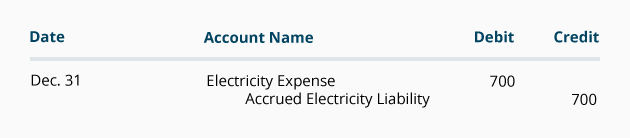

To help understand the need for accrual adjusting entries, let’s assume a service company began operations on December 3. It uses lots of electricity and its accounting periods end on the last day of every month. The electricity used by the company in December is billed by the electric utility after reading the meter on January 2. Based on the meter reading, the electricity bill for December’s usage is $675. The company receives and records the bill on January 10 and will pay the bill when due on January 27.

Without an accrual adjusting entry, the company’s general ledger accounts as of December 31 will not contain any amount for the electricity it used in December. Therefore, without an accrual adjusting entry dated December 31, the company’s balance sheet will not report a liability for the amount owed for the electricity used during December. Further, the company’s income statement will report $0 electricity expense for December.

NOTE: Without an accrual adjusting entry dated December 31, the financial statements for December will not reflect reality.

If the actual cost of the electricity used in December is not available when preparing the December financial statements, the amount must be estimated. Let’s assume that in our example the company estimated the electricity cost for December was $700. Therefore, the accrual adjusting entry will be:

(While we prefer precision, recording the estimate of $700 is far better than reporting no cost or delaying the financial statements until the exact amount is known.)

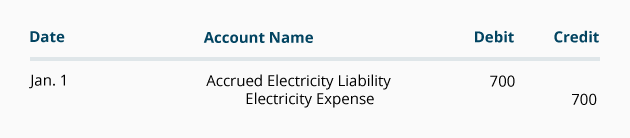

Since the actual electricity bill will be received and processed in January, the estimated amount must be replaced with the actual amount. Therefore, on the first day of the next accounting period, the company will remove the accrual of $700 by recording the following reversing entry:

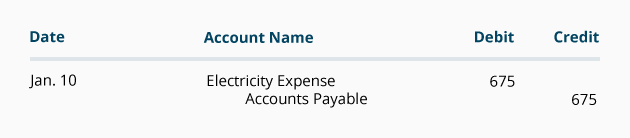

The use of reversing entries allows the bookkeeper or accounts payable clerk to follow the normal routine for recording the actual vendor invoices. (There’s no need to determine whether some or all of the actual bill/invoice had been recorded earlier using an adjusting entry.) Therefore on January 10, the actual electricity bill of $675 will be recorded as follows:

Introduction

In addition to the required annual financial statements, companies often prepare interim financial statements for shorter periods (quarterly, monthly, year-to-date, 26 weeks, etc.). Accountants assume that a company’s ongoing operations and activities can be divided into these relatively short time periods even though the company will be in the middle of complex processes and projects.

Further, some of the transaction amounts already recorded in the general ledger accounts pertain to multiple accounting periods (past, current, and/or future). Still other transactions (expenses and/or revenues) have occurred but won’t get recorded until the following accounting period.

As a result, adjusting entries must be recorded at the end of each accounting period to:

- Defer some recorded amounts to a later accounting period (deferral adjusting entries)

- Record items that are not yet recorded but they pertain to the current accounting period (accrual adjusting entries)

Basically, adjusting entries are necessary for the company’s financial statements to reflect the accrual method of accounting (not simply the cash method). Using the accrual method means the company’s:

- Balance sheet will report all the company’s assets and liabilities at the end of the accounting period

- Income statement will report only the revenues earned and only the expenses incurred during the accounting period

WATCH NOW

Advance Your Career with Our PRO Training

Adjusting Entries in General

As is the case with all accounting entries (in a double-entry accounting and bookkeeping system) there must be a minimum of two general ledger accounts, and the total of the debit amounts must equal the total of the credit amounts.

Each adjusting entry:

- Will involve a balance sheet account and an income statement account

- Is dated using the final date of the accounting period (year, month, etc.)

Adjusting entries are often categorized as follows:

- Accrual adjusting entries or accruals which involve transactions that occurred during the accounting period, but the amounts are not yet recorded in the general ledger accounts as of the final moment of the accounting period.

- Deferral adjusting entries or deferrals which involve amounts already recorded in the accounts, but some or all of the amounts must be deferred to a future accounting period’s income statement.

- Other adjusting entries include the period’s depreciation of assets used in the business, estimated losses relating to uncollectible receivables, changes to the carrying value of certain assets, and others.

Reversing Entries

Reversing entries are recorded on the first day of the period that follows the date of the accrual adjusting entries. Assume a company records an accrual adjusting entry dated December 31 for $500 of interest expense that it incurred in December. The accrual adjusting entry will be reversed (undone) using the date of January 1.

The use of reversing entries:

- Prevents reporting an accrued expense or revenue twice: once with the accrual adjusting entry, and then again when the actual documents are processed.

- Saves a bookkeeper’s or accounting clerk’s time in the accounting period after the accrual adjusting entries. There will be no need to investigate whether each document being processed had some or all of the amount already recorded with an accrual adjusting entry using the last date of the previous period.

NOTE:

AccountingCoach’s explanations, tests, etc. assume the accrual method of accounting is being used for each company’s financial statements. This is consistent with most financial accounting textbooks.

You should be aware that AccountingCoach and most financial accounting courses do NOT discuss how a company’s transactions will be reported on a company’s income tax return. There may be differences between the amounts to be reported on a company’s financial statements and the amounts to be reported on a company’s income tax return.

For example, a small business may be able to use the cash method (basis) of accounting on its income tax return. However, the management and owners of the business are better served using the accrual method of accounting on its financial statements.

Further, the Internal Revenue Service (IRS) allows a company’s tax return to expense the cost of certain assets faster than the depreciation expense reported on the company’s financial statements.

For these and other differences you should consult with your tax adviser or search www.IRS.gov regarding income tax reporting.

Adjusting Entries are Necessary for the Accrual Method of Accounting

Adjusting entries are required at the end of each accounting period so that each period’s financial statements reflect the accrual method of accounting. The accrual method of accounting means a company’s:

- Income statements will report only (and all) the revenues the company earned during the accounting period (not simply the cash amounts received).To achieve this, a company will record adjusting entries using the date of the last day in the accounting period. The adjusting entry to accrue revenues will involve an income statement account and a related balance sheet account such as Accrued Receivables.

- Income statements should also report only (and all) the expenses the company incurred during the accounting period (not simply the cash amounts paid).To achieve this, a company records adjusting entries using the date of the last day in the accounting period. The adjusting entry to accrue expenses will involve an income statement account and a related balance sheet account such as Accrued Liabilities.

- Balance sheets should report all the company’s assets and liabilities as of the final moment of the period. Some of the asset and liability amounts may be related to accrual adjusting entries needed to report the period’s revenues and expenses, and some may involve a loss that is probable and the amount can be estimated.

It is helpful to keep in mind that each adjusting entry includes a balance sheet account and an income statement account. Thanks to double-entry accounting, the company’s balance sheet amounts and income statement amounts are connected.

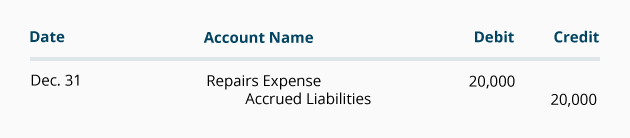

For instance, if a company had an emergency repair on December 29 but the repair transaction was not recorded in the accounts as of December 31, the accrual method of accounting requires an accrual adjusting entry dated December 31 that:

- Increases the amount of the period’s repair expenses (that will be reported on the income statement), and

- Increases the liabilities at the end of the period (that will be reported on the balance sheet).

Why Reversing Entries are Used with Accrual Adjusting Entries

Assume that on December 29, ABCO required an emergency repair at a cost of $20,000. However, ABCO did not receive the bill/invoice by the time the December 31 financial statements were prepared. Therefore, an accrual adjusting entry must be recorded by ABCO as of December 31. (The adjusting entry will record the $20,000 expense and the $20,000 liability.)

No doubt, ABCO will receive the $20,000 bill or invoice in early January.

To avoid reporting the $20,000 expense twice (once with the accrual adjusting entry and again when the actual bill is received and processed in January), ABCO will remove the December 31 accrual adjusting entry after the December 31 financial statements are distributed. This is done with a reversing entry dated January 1 or 2.

The reversing entry is a huge time saver when the invoices and bills received and processed in January are recorded. In our example, the bookkeeper or accounts payable clerk will be able to process the $20,000 repair bill by simply debiting Repairs Expense and crediting Accounts Payable. There will be no fear of recording the $20,000 twice (since the accrued amounts from the December 31 accrual adjusting entry will have been removed with the reversing entry dated January 1 or 2.

In the remainder of this explanation, we will demonstrate how accrual adjusting entries are recorded and reversed, and what occurs in the general ledger accounts.

Understanding a Reversing Entry for an Accrued Expense

Through the use of T-accounts, you will see what is occurring when an accrual adjusting entry and the related reversing entry are recorded. We will use the following information:

|

Entry #1.

|

An accrual adjusting entry dated December 31 is needed for a repair that occurred on December 29, but was not yet recorded in the general ledger accounts

|

|

Entry #2.

|

The closing entry for the Repairs Expense account is recorded as of December 31

|

|

Entry #3.

|

The closing entry for the Income Summary account is recorded as of December 31

|

|

Entry #4.

|

The reversing entry is recorded as of January 1

|

|

Entry #5.

|

The processing/recording of the actual vendor invoice occurs on January 6

|

| Entry #6. |

The routine payment of the vendor’s invoice occurs on January 20 |

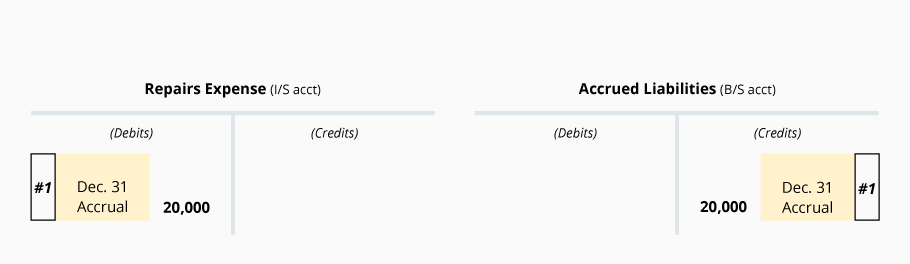

Entry #1: An accrual adjusting entry for a repair expense that was incurred but not yet recorded

Assume that the company ABCO required an emergency repair on December 29 but had not received a bill/invoice from the contractor as of December 31, (the end of ABCO’s accounting year). For ABCO’s financial statements to comply with the accrual method of accounting, an accrual adjusting entry dated December 31, must be recorded for the repair’s known (or estimated) cost of $20,000.

The accrual adjusting entry will result in ABCO’s December income statement (I/S) reporting the December repair expense of $20,000 in the period when it occurred. In addition, ABCO’s December 31 balance sheet (B/S) will report the $20,000 obligation as a current liability of $20,000.

ABCO’s accrual adjusting entry on December 31 will be:

This accrual adjusting entry is shown as #1 in the following T-accounts:

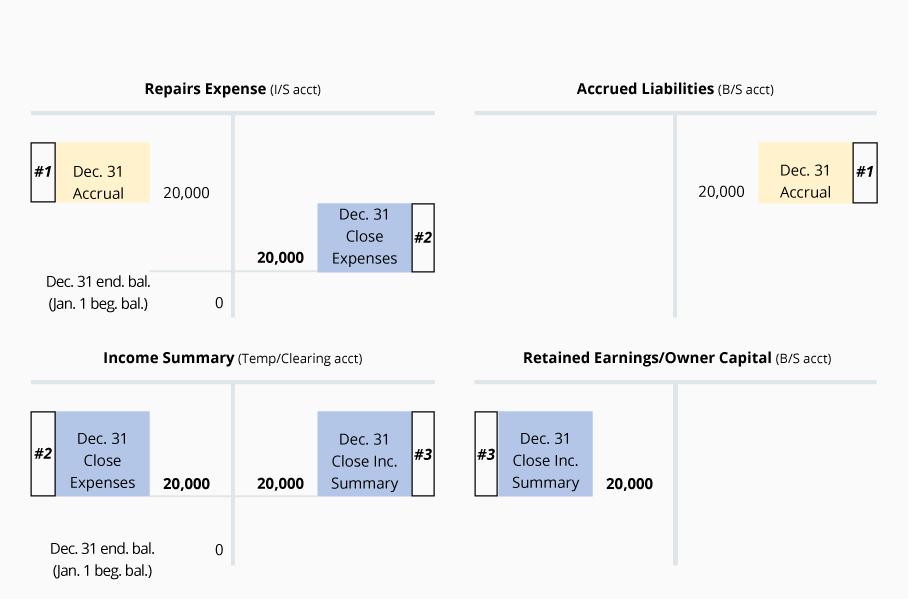

Entry #2 and Entry #3: Closing entries on December 31.

To illustrate closing entries, let’s assume that ABCO uses a manual accounting system. After ABCO’s December 31 financial statements are prepared, closing entries will move the balances from the (temporary) income statement accounts to a (permanent) balance sheet account. The balance sheet account at a corporation is Retained Earnings. The balance sheet account at a sole proprietorship is the Owner’s Capital account.

To simplify our explanation of reversing entries, lets assume Accrual Adjusting Entry #1 represents ABCO’s only transaction for the year ending on December 31. Therefore, ABCO will have the following closing entries:

- Closing Entry #2 transfers the $20,000 ending balance from the account Repairs Expense to the temporary clearing account Income Summary.

- Closing Entry #3 transfers the debit balance from the Income Summary account to the

Retained Earnings account (if a corporation) or to the Owner’s Capital account (if a sole proprietorship).

The closing entries will cause the account Repairs Expense to begin the next accounting period with a $0 balance, as shown in the following T-accounts:

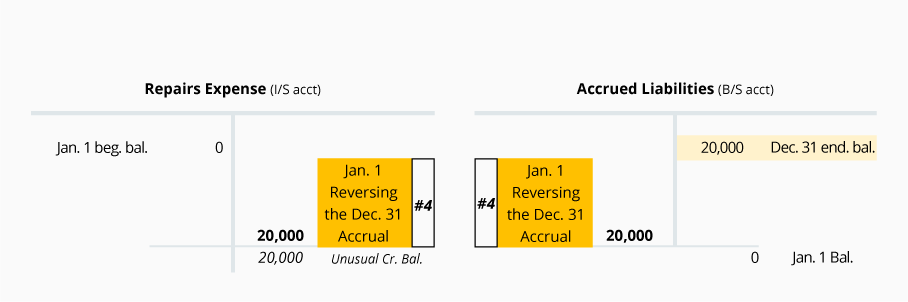

Entry #4: Reversing entry for the accrued repair expense

Reversing entries are recorded using the date at the beginning of the accounting period that follows the accrual adjusting entry. The following entry reverses the accrual Entry #1 from Dec. 31:

The reversing entry dated January 1, is shown as #4 in the following T-accounts:

The reversing entry’s credit to Repairs Expense on January 1 will temporarily result in the unusual credit balance in Repairs Expense.

Recall that the accrual adjusting entry of $20,000 was debited to Repairs Expense and credited to Accrued Liabilities. This was necessary so ABCO’s December income statement reported the expense, and the December 31 balance sheet reported the liability.

The $20,000 repair expense cannot be reported in both December and again in January. The reversing entry prevents this from occurring. As a result, there is no need for the person processing the vendors’ invoices during January to do anything other than debit Repairs Expense and credit Accounts Payable.

The following T-accounts for ABCO illustrate the reversing entry of January 1, which temporarily results in the account Repairs Expense having the unusual credit balance. This credit balance will offset the amount that will be recorded when the actual vendor’s invoice is processed. This prevents double-counting the $20,000 repair that occurred on December 29.

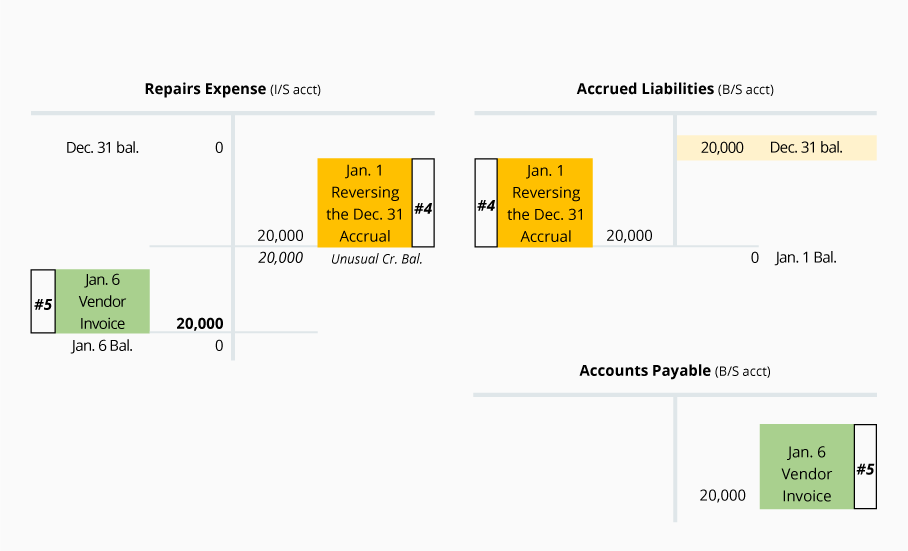

Entry #5: Processing the vendor’s invoice on January 6.

Note that on January 6, when the vendor’s invoice is processed and recorded in ABCO’s general ledger accounts, Entry #5 credits Accounts Payable for the actual amount of the invoice (which we will assume was exactly $20,000).

[When the actual amount of the invoice is greater or is less than the estimated amount in the adjusting and reversing entries, the actual amount of the invoice will be recorded when the invoice is processed. These differences are usually small and will simply mean a small difference in the Repairs Expense for January.]

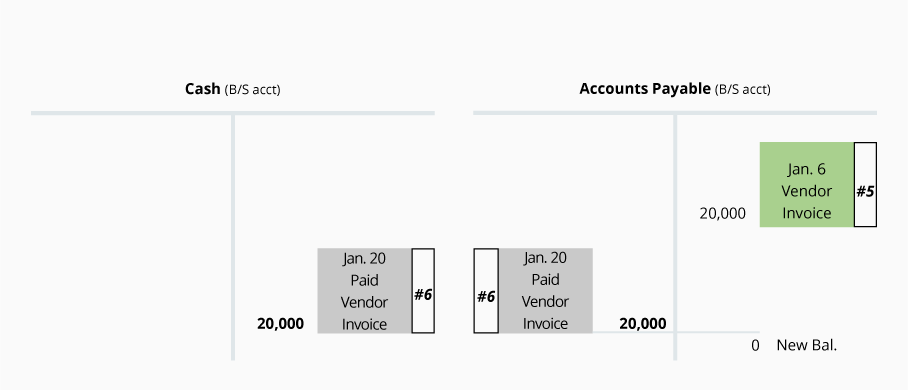

Entry #6: Payment of vendor’s invoice on January 20.

On January 20, when ABCO pays the vendor, it will pay the actual amount owed. Our T-accounts assume that the actual amount owed was $20,000. This means that ABCO debits Accounts Payable and credits Cash for $20,000 as shown here:

Understanding a Reversing Entry for Accrued Service Revenue

Assume that REVCO began operations on December 1, and its accounting year will be the calendar year ending on December 31. Its financial statements are based on the accrual method of accounting. REVCO’s billing policy is to invoice its clients on the 15th day following the month when the services were provided.

On December 20, REVCO completed $4,000 of services for XLCO (its only client in December). Therefore, as of December 31, REVCO earned $4,000 of service revenue (that will be invoiced on January 15) and it has earned the right to a receivable (an asset) of $4,000.

We will demonstrate with T-accounts how the following entries will affect the general ledger accounts:

|

Entry #1.

|

The accrual adjusting entry dated December 31 to record the revenue and the receivable that were earned but not yet recorded in the general ledger accounts

|

|

Entry #2.

|

The closing entry for the revenue account at the end of December 31

|

|

Entry #3.

|

The closing entry for the income summary account at the end of December 31

|

|

Entry #4.

|

The January 1 reversing entry pertaining to the December 31 accrual adjusting entry

|

|

Entry #5.

|

The routine processing/recording of the REVCO’s sales invoice on January 15

|

| Entry #6. |

The routine entry to record the January 20 receipt for the January 15 invoice |

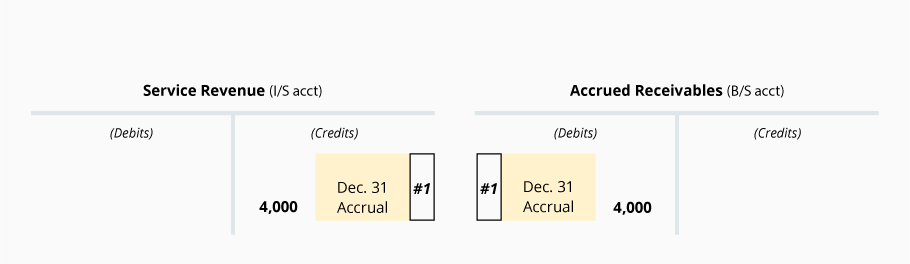

Entry #1: The accrual adjusting entry for the service revenue and the receivable earned but not yet recorded in the accounts as of December 31.

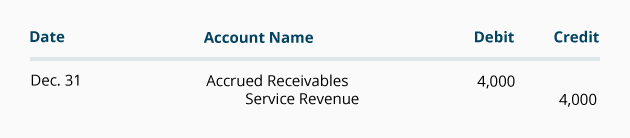

As of December 31, REVCO must prepare an accrual adjusting entry so that:

- Its income statement (I/S) will report the $4,000 of revenue that was earned during December.

- Its December 31 balance sheet (B/S) will report the $4,000 receivable (a current asset).

Therefore, REVCO’s accrual adjusting entry on December 31 will be:

This accrual adjusting entry appears as #1 in the following T-accounts:

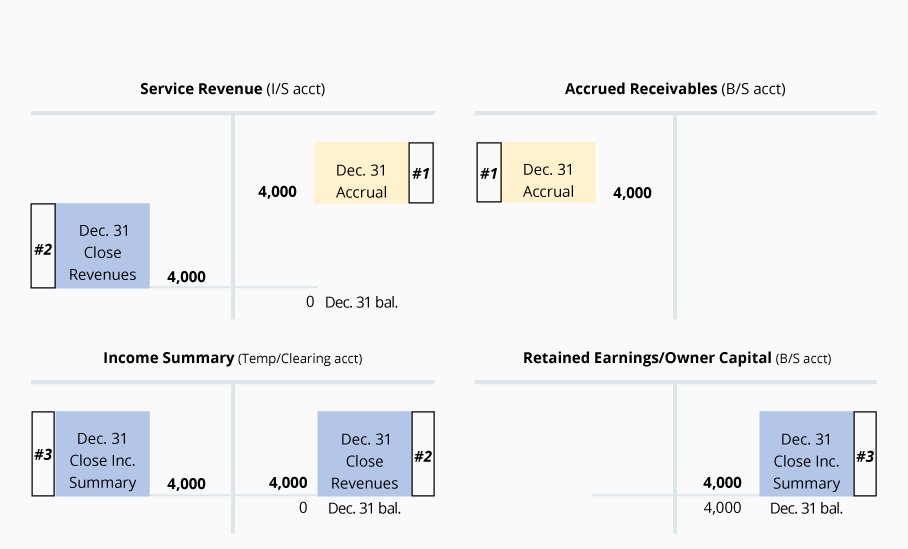

Entry #2: The closing entry for the revenue account at the end of December 31.

Entry #3: The closing entry for the income summary account at the end of December 31.

In a manual accounting system (after REVCO’s December 31 financial statements are prepared), closing entries will move the balances from the temporary accounts to a permanent account within the stockholders’ equity or owner’s equity section of the balance sheet.

Entry #4: Reversing entry for the accrued service revenue

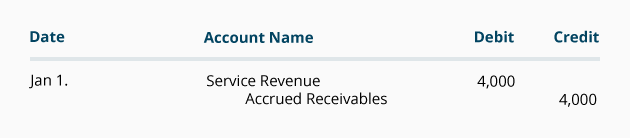

Reversing entries are recorded on Day 1 of the accounting period after the accrual adjusting entry. Therefore, REVCO’s reversing entry is dated January 1. The following entry reverses the accrual Entry #1 from Dec. 31:

The January 1 reversing entry is shown as #4 in the following T-accounts:

REVCO’s reversing entry (Entry #4) on January 1 removes the December 31 accrual adjusting entry’s $4,000 credit to Service Revenue and the $4,000 debit to Accrued Receivables (Entry #1). In effect, REVCO is removing the adjusting entry amounts to make way for REVCO’s actual sales invoice of January 15.

The January 1 reversing entry also simplifies the bookkeeper’s job when recording the January sales invoices. The bookkeeper can credit Service Revenue for the total amount of the sales invoices without investigating whether the January sales invoices include amounts that were earned and had been recorded in the December 31 accrual adjusting entries.

Entry #5: Processing the REVCO’s sales invoice on January 15

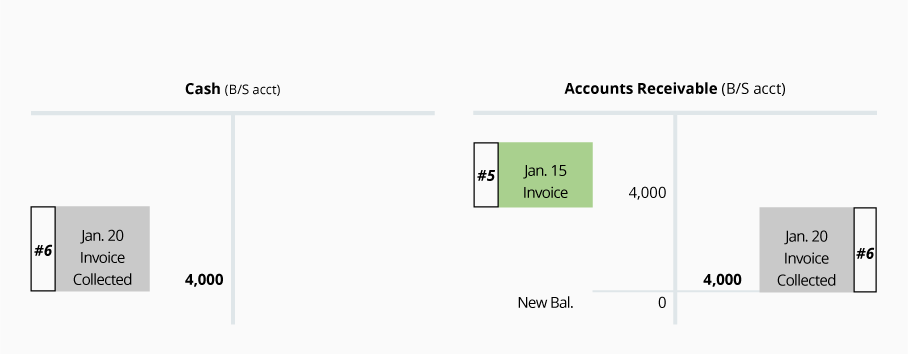

The following T-accounts for REVCO illustrate the reversing entry dated January 1 (Entry #4). After the reversing entry is recorded, the account Service Revenue has the unusual debit balance of $4,000. This debit balance will offset the amount that will be recorded when the January 15 sales invoice is processed. As a result, the $4,000 that was in the accrual adjusting entry on December 31 will not be double-counted when the January 15 sales invoice is recorded.

Note that on January 15, when REVCO processes its sales invoice, Entry #5 debits Accounts Receivable and credits Service Revenue with the actual amount of the sales invoice. This is what the bookkeeper or accounting clerk does when routinely processing/recording all of the sales invoices.

[If the amount of the January 15 sales invoice ended up being slightly more (or less) than the accrued $4,000, the actual amount of the sales invoice will be recorded on January 15. The small difference will be reported in the January financial statements. Accountants will not reissue December’s financial statements for relatively small “changes in estimates”.]

Entry 6: Recording REVCO’s collection of its accounts receivable on January 20

On January 20, when REVCO collects the amount owed from the customer for the January 15 sales invoice, REVCO will debit Cash and will credit Accounts Receivable as shown by Entry #6 in the following T-accounts:

Disclaimer

You should consider our materials to be an introduction to selected accounting and bookkeeping topics (with complexities likely omitted). We focus on financial statement reporting and do not discuss how that differs from income tax reporting. Therefore, you should always consult with accounting and tax professionals for assistance with your specific circumstances.

Earn Our Certificate

for This Topic

When you join PRO, you will receive instant access to 16 different Certificates of Achievement plus our Bookkeeping Certificate of Excellence.

View PRO Features